48 CFR § 52.232-23 - Assignment of Claims.

As prescribed in 32.806(a)(1) , insert the following clause:

(a) The Contractor, under the Assignment of Claims Act, as amended, 31 U.S.C. 3727 , 41 U.S.C. 6305 (hereafter referred to as the Act ), may assign its rights to be paid amounts due or to become due as a result of the performance of this contract to a bank, trust company, or other financing institution, including any Federal lending agency . The assignee under such an assignment may thereafter further assign or reassign its right under the original assignment to any type of financing institution described in the preceding sentence.

(b) Any assignment or reassignment authorized under the Act and this clause shall cover all unpaid amounts payable under this contract, and shall not be made to more than one party, except that an assignment or reassignment may be made to one party as agent or trustee for two or more parties participating in the financing of this contract.

(c) The Contractor shall not furnish or disclose to any assignee under this contract any classified document (including this contract) or information related to work under this contract until the Contracting Officer authorizes such action in writing.

Alternate I (APR 1984). If a no-setoff commitment is to be included in the contract (see 32.801 and 32.803(d) ), add the following sentence at the end of paragraph (a) of the basic clause:

Unless otherwise stated in this contract, payments to an assignee of any amounts due or to become due under this contract shall not, to the extent specified in the Act, be subject to reduction or setoff.

In The (Red)

The Business Bankruptcy Blog

Assignments For The Benefit Of Creditors: Simple As ABC?

Companies in financial trouble are often forced to liquidate their assets to pay creditors. While a Chapter 11 bankruptcy sometimes makes the most sense, other times a Chapter 7 bankruptcy is required, and in still other situations a corporate dissolution may be best. This post examines another of the options, the assignment for the benefit of creditors, commonly known as an "ABC."

A Few Caveats . It’s important to remember that determining which path an insolvent company should take depends on the specific facts and circumstances involved. As in many areas of the law, one size most definitely does not fit all for financially troubled companies. With those caveats in mind, let’s consider one scenario sometimes seen when a venture-backed or other investor-funded company runs out of money.

One Scenario . After a number of rounds of investment, the investors of a privately held corporation have decided not to put in more money to fund the company’s operations. The company will be out of cash within a few months and borrowing from the company’s lender is no longer an option. The accounts payable list is growing (and aging) and some creditors have started to demand payment. A sale of the business may be possible, however, and a term sheet from a potential buyer is anticipated soon. The company’s real property lease will expire in nine months, but it’s possible that a buyer might want to take over the lease.

- A Chapter 11 bankruptcy filing is problematic because there is insufficient cash to fund operations going forward, no significant revenues are being generated, and debtor in possession financing seems highly unlikely unless the buyer itself would make a loan.

- The board prefers to avoid a Chapter 7 bankruptcy because it’s concerned that a bankruptcy trustee, unfamiliar with the company’s technology, would not be able to generate the best recovery for creditors.

The ABC Option . In many states, another option that may be available to companies in financial trouble is an assignment for the benefit of creditors (or "general assignment for the benefit of creditors" as it is sometimes called). The ABC is an insolvency proceeding governed by state law rather than federal bankruptcy law.

California ABCs . In California, where ABCs have been done for years, the primary governing law is found in California Code of Civil Procedure sections 493.010 to 493.060 and sections 1800 to 1802 , among other provisions of California law. California Code of Civil Procedure section 1802 sets forth, in remarkably brief terms, the main procedural requirements for a company (or individual) making, and an assignee accepting, a general assignment for the benefit of creditors:

1802. (a) In any general assignment for the benefit of creditors, as defined in Section 493.010, the assignee shall, within 30 days after the assignment has been accepted in writing, give written notice of the assignment to the assignor’s creditors, equityholders, and other parties in interest as set forth on the list provided by the assignor pursuant to subdivision (c). (b) In the notice given pursuant to subdivision (a), the assignee shall establish a date by which creditors must file their claims to be able to share in the distribution of proceeds of the liquidation of the assignor’s assets. That date shall be not less than 150 days and not greater than 180 days after the date of the first giving of the written notice to creditors and parties in interest. (c) The assignor shall provide to the assignee at the time of the making of the assignment a list of creditors, equityholders, and other parties in interest, signed under penalty of perjury, which shall include the names, addresses, cities, states, and ZIP Codes for each person together with the amount of that person’s anticipated claim in the assignment proceedings.

In California, the company and the assignee enter into a formal "Assignment Agreement." The company must also provide the assignee with a list of creditors, equityholders, and other interested parties (names, addresses, and claim amounts). The assignee is required to give notice to creditors of the assignment, setting a bar date for filing claims with the assignee that is between five to six months later.

ABCs In Other States . Many other states have ABC statutes although in practice they have been used to varying degrees. For example, ABCs have been more common in California than in states on the East Coast, but important exceptions exist. Delaware corporations can generally avail themselves of Delaware’s voluntary assignment statutes , and its procedures have both similarities and important differences from the approach taken in California. Scott Riddle of the Georgia Bankruptcy Law Blog has an interesting post discussing ABC’s under Georgia law . Florida is another state in which ABCs are done under specific statutory procedures . For an excellent book that has information on how ABCs are conducted in various states, see Geoffrey Berman’s General Assignments for the Benefit of Creditors: The ABCs of ABCs , published by the American Bankruptcy Institute .

Important Features Of ABCs . A full analysis of how ABCs function in a particular state and how one might affect a specific company requires legal advice from insolvency counsel. The following highlights some (but by no means all) of the key features of ABCs:

- Court Filing Issue . In California, making an ABC does not require a public court filing. Some other states, however, do require a court filing to initiate or complete an ABC.

- Select The Assignee . Unlike a Chapter 7 bankruptcy trustee, who is randomly appointed from those on an approved panel, a corporation making an assignment is generally able to choose the assignee.

- Shareholder Approval . Most corporations require both board and shareholder approval for an ABC because it involves the transfer to the assignee of substantially all of the corporation’s assets. This makes ABCs impractical for most publicly held corporations.

- Liquidator As Fiduciary . The assignee is a fiduciary to the creditors and is typically a professional liquidator.

- Assignee Fees . The fees charged by assignees often involve an upfront payment and a percentage based on the assets liquidated.

- No Automatic Stay . In many states, including California, an ABC does not give rise to an automatic stay like bankruptcy, although an assignee can often block judgment creditors from attaching assets.

- Event Of Default . The making of a general assignment for the benefit of creditors is typically a default under most contracts. As a result, contracts may be terminated upon the assignment under an ipso facto clause .

- Proof Of Claim . For creditors, an ABC process generally involves the submission to the assignee of a proof of claim by a stated deadline or bar date, similar to bankruptcy. (Click on the link for an example of an ABC proof of claim form .)

- Employee Priority . Employee and other claim priorities are governed by state law and may involve different amounts than apply under the Bankruptcy Code. In California, for example, the employee wage and salary priority is $4,300, not the $10,950 amount currently in force under the Bankruptcy Code.

- 20 Day Goods . Generally, ABC statutes do not have a provision similar to that under Bankruptcy Code Section 503(b)(9) , which gives an administrative claim priority to vendors who sold goods in the ordinary course of business to a debtor during the 20 days before a bankruptcy filing . As a result, these vendors may recover less in an ABC than in a bankruptcy case, subject to assertion of their reclamation rights .

- Landlord Claim . Unlike bankruptcy, there generally is no cap imposed on a landlord’s claim for breach of a real property lease in an ABC.

- Sale Of Assets . In many states, including California, sales by the assignee of the company’s assets are completed as a private transaction without approval of a court. However, unlike a bankruptcy Section 363 sale , there is usually no ability to sell assets "free and clear" of liens and security interests without the consent or full payoff of lienholders. Likewise, leases or executory contracts cannot be assigned without required consents from the other contracting party.

- Avoidance Actions . Most states allow assignees to pursue preferences and fraudulent transfers. However, the U.S. Court of Appeals for the Ninth Circuit has held that the Bankruptcy Code pre-empts California’s preference statute , California Code of Civil Procedure section 1800. Nevertheless, to date the California state courts have refused to follow the Ninth Circuit’s decision and still permit assignees to sue for preferences in California state court . In February 2008, a Delaware state court followed the California state court decisions , refusing either to follow the Ninth Circuit position or to hold that the California preference statute was pre-empted by the Bankruptcy Code. The Delaware court was required to apply California’s ABC preference statute because the avoidance action arose out of an earlier California ABC.

The Scenario Revisited. With this overview in mind, let’s return to our company in distress.

- The prospect of a term sheet from a potential buyer may influence whether our hypothetical company should choose an ABC or another approach. Some buyers will refuse to purchase assets outside of a Chapter 11 bankruptcy or a Chapter 7 case. Others are comfortable with the ABC process and believe it provides an added level of protection from fraudulent transfer claims compared to purchasing the assets directly from the insolvent company. Depending on the value to be generated by a sale, these considerations may lead the company to select one approach over the other available options.

- In states like California where no court approval is required for a sale, the ABC can also mean a much faster closing — often within a day or two of the ABC itself provided that the assignee has had time to perform due diligence on the sale and any alternatives — instead of the more typical 30-60 days required for bankruptcy court approval of a Section 363 sale. Given the speed at which they can be done, in the right situation an ABC can permit a "going concern" sale to be achieved.

- Secured creditors with liens against the assets to be sold will either need to be paid off through the sale or will have to consent to release their liens; forced "free and clear" sales generally are not possible in an ABC.

- If the buyer decides to take the real property lease, the landlord will need to consent to the lease assignment. Unlike bankruptcy, the ABC process generally cannot force a landlord or other third party to accept assignment of a lease or executory contract.

- If the buyer decides not to take the lease, or no sale occurs, the fact that only nine months remains on the lease means that this company would not benefit from bankruptcy’s cap on landlord claims. If the company’s lease had years remaining, and if the landlord were unwilling to agree to a lease termination approximating the result under bankruptcy’s landlord claim cap, the company would need to consider whether a bankruptcy filing was necessary to avoid substantial dilution to other unsecured creditor claims that a large, uncapped landlord claim would produce in an ABC.

- If the potential buyer walks away, the assignee would be responsible for determining whether a sale of all or a part of the assets was still possible. In any event, assets would be liquidated by the assignee to the extent feasible and any proceeds would be distributed to creditors in order of their priority through the ABC’s claims process.

- While other options are available and should be explored, an ABC may make sense for this company depending upon the buyer’s views, the value to creditors and other constituencies that a sale would produce, and a clear-eyed assessment of alternative insolvency methods.

Conclusion . When weighing all of the relevant issues, an insolvent company’s management and board would be well-served to seek the advice of counsel and other insolvency professionals as early as possible in the process. The old song may say that ABC is as "easy as 1-2-3," but assessing whether an assignment for the benefit of creditors is best for an insolvent company involves the analysis of a myriad of complex factors.

The Federal Register

The daily journal of the united states government, request access.

Due to aggressive automated scraping of FederalRegister.gov and eCFR.gov, programmatic access to these sites is limited to access to our extensive developer APIs.

If you are human user receiving this message, we can add your IP address to a set of IPs that can access FederalRegister.gov & eCFR.gov; complete the CAPTCHA (bot test) below and click "Request Access". This process will be necessary for each IP address you wish to access the site from, requests are valid for approximately one quarter (three months) after which the process may need to be repeated.

An official website of the United States government.

If you want to request a wider IP range, first request access for your current IP, and then use the "Site Feedback" button found in the lower left-hand side to make the request.

- Copley Library

- Legal Research Center

Home > School of Law > Law School Journals > SDLR > Vol. 53 > Iss. 3 (2016)

San Diego Law Review

Notice and the claim presentation requirements under the california government claims act: recalibrating the scales of justice.

Samantha Lewis

Library of Congress Authority File

http://id.loc.gov/authorities/names/n79122466

Document Type

To recalibrate the scales of justice, this Comment advocates for a statutory amendment that encompasses two changes. First, the amendment would require plaintiffs to present their government claims against the state directly to the public entity that allegedly caused the harm, instead of the VCGCB, thereby accomplishing the statute’s objective of providing notice to the state entity. Second, instead of the VCGCB assessing claims against the state, each state agency would have its own government claims office (GCO) handle government claims for the respective individualized entity. This would promote efficiency in the government claims process by cutting out the “middleman,” the VCGCB. Moreover, this amendment would ensure that plaintiffs avoid a fatal loss of substantive rights due to a minor procedural technicality, one that does not achieve the statute’s legislative purpose of providing state entities with notice of potential lawsuits.

Part II of this Comment provides a brief history of the Act, an overview of the current process for filing government claims against the state of California, including the VCGCB’s role in that process, and the consequences for failing to comply with the claim presentation statutes, specifically focusing on Government Code section 915, subdivision (b). Part III discusses the legislative intent underlying section 915’s claim presentation requirements and examines how the requirements are inconsistent with the statute’s purpose. Part IV discusses California courts’ varying interpretations and applications of the strict claim presentation requirement under section 915, subdivision (b), specifically focusing on two California decisions: Jamison v. State of California (Jamison) and DiCampli-Mintz v. County of Santa Clara (DiCampli-Mintz). Part IV also discusses the doctrine of substantial compliance and analyzes how these two California decisions vary in their applications of the doctrine. Part V explains the need to reconcile the Jamison and DiCampli-Mintz decisions. Part VI discusses potential ways to reconcile these cases, and provides the statutory language and benefits of the superior solution. Finally, Part VII concludes by summarizing the consequences of California’s current Government Code section 915, while highlighting the beneficial impact the proposed statutory amendment would have on the legal system.

Recommended Citation

Samantha Lewis, Notice and the Claim Presentation Requirements Under the California Government Claims Act: Recalibrating the Scales of Justice , 53 S an D iego L. R ev. 701 (2016). Available at: https://digital.sandiego.edu/sdlr/vol53/iss3/6

Since October 30, 2018

Included in

State and Local Government Law Commons

- Journal Home

- Most Popular Papers

- Receive Email Notices or RSS

Advanced Search

ISSN: 0036-4037

Home | About | FAQ | My Account | Accessibility Statement

Privacy Copyright

FAC Number: 2024-03 Effective Date: 02/23/2024

32.805 Procedure.

(a) Assignments.

(1) Assignments by corporations shall be-

(i) Executed by an authorized representative;

(ii) Attested by the secretary or the assistant secretary of the corporation; and

(iii) Impressed with the corporate seal or accompanied by a true copy of the resolution of the corporation’s board of directors authorizing the signing representative to execute the assignment.

(2) Assignments by a partnership may be signed by one partner, if the assignment is accompanied by adequate evidence that the signer is a general partner of the partnership and is authorized to execute assignments on behalf of the partner-ship.

(3) Assignments by an individual shall be signed by that individual and the signature acknowledged before a notary public or other person authorized to administer oaths.

(b) Filing. The assignee shall forward to each party specified in 32.802 (e) an original and three copies of the notice of assignment, together with one true copy of the instrument of assignment. The true copy shall be a certified duplicate or photostat copy of the original assignment.

(c) Format for notice of assignment. The following is a suggested format for use by an assignee in providing the notice of assignment required by 32.802 (e).

Notice of Assignment

To: ___________ [ Address to one of the parties specified in 32.802 (e) ].

This has reference to Contract No. __________ dated ______, entered into between ______ [ Contractor’s name and address ] and ______ [ Government agency, name of office, and address ], for ________ [ Describe nature of the contract ].

Moneys due or to become due under the contract described above have been assigned to the undersigned under the provisions of the Assignment of Claims Act of1940, as amended, ( 31 U.S.C.3727 , 41 U.S.C.6305 ).

A true copy of the instrument of assignment executed by the Contractor on ___________ [ Date ], is attached to the original notice.

Payments due or to become due under this contract should be made to the undersigned assignee.

Please return to the undersigned the three enclosed copies of this notice with appropriate notations showing the date and hour of receipt, and signed by the person acknowledging receipt on behalf of the addressee.

Very truly yours,

__________________________________________________ [ Name of Assignee ]

By _______________________________________________ [ Signature of Signing Officer ]

__________________________________________________ [ Titleof Signing Officer ]

__________________________________________________ [ Address of Assignee ]

Acknowledgement

Receipt is acknowledged of the above notice and of a copy of the instrument of assignment. They were received ____(a.m.) (p.m.) on ______, 20___.

__________________________________________________ [ Signature ]

__________________________________________________ [ Title ]

__________________________________________________ On behalf of

__________________________________________________ [ Name of Addressee of this Notice ]

(d) Examination by the Government. In examining and processing notices of assignment and before acknowledging their receipt, contracting officers should assure that the following conditions and any additional conditions specified in agency regulations, have been met:

(1) The contract has been properly approved and executed.

(2) The contract is one under which claims may be assigned.

(3) The assignment covers only money due or to become due under the contract.

(4) The assignee is registered separately in the System for Award Management unless one of the exceptions in 4.1102 applies.

(e) Release of assignment.

(1) A release of an assignment is required whenever-

(i) There has been a further assignment or reassignment under the Act; or

(ii) The contractor wishes to reestablish its right to receive further payments after the contractor’s obligations to the assignee have been satisfied and a balance remains due under the contract.

(2) The assignee, under a further assignment or reassignment, in order to establish a right to receive payment from the Government, must file with the addressees listed in 32.802 (e) a-

(i) Written notice of release of the contractor by the assigning financing institution;

(ii) Copy of the release instrument;

(iii) Written notice of the further assignment or reassignment; and

(iv) Copy of the further assignment or reassignment instrument.

(3) If the assignee releases the contractor from an assignment of claims under a contract, the contractor, in order to establish a right to receive payment of the balance due under the contract, must file a written notice of release together with a true copy of the release of assignment instrument with the addressees noted in 32.802 (e).

(4) The addressee of a notice of release of assignment or the official acting on behalf of that addressee shall acknowledge receipt of the notice.

Definitions

FAC Changes

Style Formatter

- Data Initiatives

- Regulations

- Smart Matrix

- Regulations Search

- Acquisition Regulation Comparator (ARC)

- Large Agencies

- Small Agencies

- CAOC History

- CAOC Charter

- Civilian Agency Acquisition Council (CAAC)

- Federal Acquisition Regulatory Council

- Interagency Suspension and Debarment Committee (ISDC)

ACQUISITION.GOV

An official website of the General Services Administration

An official website of the United States government

Here’s how you know

The .gov means it’s official.

Federal government websites often end in .gov or .mil. Before sharing sensitive information, make sure you’re on a federal government site.

The site is secure.

The https:// ensures that you are connecting to the official website and that any information you provide is encrypted and transmitted securely.

Now Available - CBMA Importer Claims System | CBMA Import Resources

Imports – Tax Benefits under the Craft Beverage Modernization Act (CBMA)

Get Email Updates

En Français

New Provisions

The Craft Beverage Modernization Act (CBMA) provisions of the U.S. Internal Revenue Code provide for reduced rates or tax credits for beer, wine, and distilled spirits produced in or imported into the United States. These CBMA tax benefits are limited in quantity for each producer, including foreign producers. Foreign producers utilize these CBMA tax benefits by assigning them to U.S. importers of their products. U.S. importers pay the Federal excise tax on imported beer, wine, and distilled spirits, and must receive an assignment of the CBMA tax benefits from the foreign producer to take advantage of the CBMA tax benefits.

From 2018 to 2022, U.S. Customs and Border Protection (CBP) has administered the CBMA tax provisions related to imported products.

A change in the law transferred responsibility for administering the CBMA tax benefits for imported alcohol from CBP to TTB beginning with products entered for consumption in the United States on or after January 1, 2023.

The law also changed the way in which importers will take advantage of tax benefits assigned to them. Starting January 1, 2023, importers who want to take advantage of assigned tax benefits must pay the full tax rate to CBP and then subsequently submit a claim to TTB for a refund.

Hot Topics:

- CBMA Importer Claims System: Your Questions Answered

- CBMA Series: Importer Claims System Walkthrough

- CBMA Series: Preparing for Importer Claims

- CBMA Series: Overview of Foreign Producer Registration System

- TTB's Craft Beverage Modernization Act (CBMA) Imports Overview

- Read Information on Getting Started with the myTTB System

- Avoid ACE Data Errors that may Delay Payment of CBMA Importer Refund Claims

For more information:

- See TTB Industry Circular 2022-3 for updated guidance on how to calculate and use effective tax rates or standard effective tax rates (SETRs) for imported distilled spirits products that are eligible for CBMA tax benefits

- See CBP's CSMS message #54427266 of 12/20/2022 on the CBMA procedures and requirements for 2023 and after

- Access myTTB for Foreign Producer Registrations and Assignments

- View TTB's Overview of New CBMA Import Provisions webinar slides

- See TTB’s temporary rule T.D. TTB-186 , effective October 24, 2022.

- See TTB’s notice of proposed rulemaking Notice No. 215 in Docket No. TTB-2022-0009 at Regulations.gov . The comment period for the Notice closed November 22, 2022.

CBMA myTTB Data:

Foreign Producer Registrations as of February 13, 2024: 13,259

Overview for Importers ● Overview for Foreign Producers ● ACE Resources ● myTTB System User Guides ● General CBMA Import Program FAQs ● Importer Claims FAQs ● Foreign Producer Registration Questions and Answers ● CBMA Tax Benefit Assignment Questions and Answers

Summary of CBMA Import Refund Provisions for Distilled Spirits, Wine, and Beer

The following summaries outline the new provisions covering importers and foreign producers.

Overview for Importers

General: For beer, wine, and distilled spirits entered for consumption in the United States on or after January 1, 2023, an importer must pay the full rate of tax to CBP.

To take advantage of the CBMA reduced tax rates or tax credits, the importer must electronically file a refund claim with TTB. Importers may file refund claims after the close of each calendar quarter covering their entries in that quarter.

An importer cannot claim a refund unless the foreign producer of the imported beer, wine, or distilled spirits has assigned their CBMA tax benefits to that importer using the myTTB online system .

Customs Entry Filings: Before claiming a refund, the importer must submit information in their customs entry filing(s) identifying the products that will be subject to their claim, including:

- The commodity (i.e., beer, wine, or distilled spirits) and quantity (i.e., beer barrels, wine gallons, or proof gallons) being imported with an assigned CBMA tax benefit;

- The name and TTB Foreign Producer ID of the foreign producer assigning the CBMA tax benefits; and

- The specific reduced tax rate or tax credit assigned to the imported quantity.

This information is generally consistent with the information importers were required to submit to CBP to take advantage of CBMA tax benefits prior to 2023, except that TTB will use a new TTB-issued Foreign Producer ID number to identify foreign producers. See Craft Beverage Modernization Act (CBMA) – 2022 Procedures and Requirements, CSMS #50484790 (Dec. 23, 2021).

This information must be submitted electronically as part of the importer’s customs entry filing(s) in CBP’s Automated Commercial Environment (ACE). More detailed information on the entry filing requirements is available in the CBP and Trade Automated Interface Requirements (CATAIR) Entry Summary Create/Update on CBP’s website .

Importers intending to file CBMA importer refund claims must also file the TTB Message Set electronically in ACE. For instructions, see ACE Filing Instructions for TTB-Regulated Commodities | U.S. Customs and Border Protection (cbp.gov) .

Quarterly Refund Claims: An importer can file a quarterly refund claim based on CBMA tax benefits assigned to them after imported products have entered the United States for consumption, and after the importer has paid to CBP the tax due on those products at the full tax rate. Importers may not file refund claims more frequently than quarterly. That is, the calendar quarter must end before CBMA import refund claims may be filed for any consumption entries made during that quarter.

Use of myTTB Online System: Importers must submit CBMA refund claims electronically using the myTTB online system. Importers may authorize third party agents to submit filings on their behalf within the myTTB online system. Importers are responsible for ensuring that they (or their agents) have submitted accurate data in ACE before submitting a CBMA refund claim to TTB. Step-by-step instructions on filing claims are available in the Importer Claims User Guide .

Overview for Foreign Producers

General: Foreign producers may assign the CBMA tax benefits to one or more U.S. importers of their products. An importer cannot take advantage of tax benefits unless the foreign producer has assigned their tax benefits to the importer.

Quantity Limitations: By law, each foreign producer may only assign a limited quantity of tax benefits for each category of their products imported into the United States (beer, wine, or distilled spirits). Please see FAQ TB-1 for more detailed information on the quantities eligible to be assigned each calendar year.

Use of myTTB Online system : In the past, foreign producers assigned CBMA tax benefits to one or more importers using a letterhead template published by CBP. TTB will not accept letterhead assignments for calendar years 2023 and beyond. For products imported on or after January 1, 2023, foreign producers must use the myTTB online system to assign CBMA tax benefits to importers.

Foreign Producer Registration: Before assigning CBMA tax benefits, a foreign producer must first register with TTB using the online myTTB system and receive a TTB Foreign Producer ID. A foreign producer will need to provide the following information to register:

- Basic information about the business (such as business name and address) and contact information for a point of contact for the business (see FAQ FP-1 );

- Their unique U.S. Food and Drug Administration (FDA) Food Facility Registration number(s) (see FAQ FP-2 ); and

- Ownership information, if under common ownership with other foreign or U.S. alcohol producers (see FAQ FP-1 ).

When a foreign producer’s TTB registration is complete, TTB will issue a TTB Foreign Producer ID and the foreign producer will be able to make assignments through the electronic myTTB system. U.S. importers will use the TTB Foreign Producer ID to identify the foreign producer when submitting information to CBP during the entry process as well as when submitting CBMA import refund claim information to TTB.

Assigning Benefits to Importers: To assign CBMA tax benefits to importers, foreign producers will need to provide the following information:

- The calendar year for which the CBMA tax benefits are being assigned;

- The importer to whom the assignment is made, identified by TTB permit number (or TTB-assigned reference number when an importer is not required to have a TTB permit);

- The commodity (i.e. beer, wine, or distilled spirits) for which the assignment is made;

- The specific reduced tax rate or tax credit being assigned; and

- The quantity of proof gallons, wine gallons, or beer barrels on which tax benefits are being assigned.

The quantities of tax benefits available to be assigned may be impacted by controlled group rules in cases of common ownership among producers. Please see FAQs TB-1 - 2 for additional information on quantity limitations.

ACE Resources

Ace cbma tax rates table.

See the ACE CBMA Tax Rates Table . Use these codes for consumption entries on or after January 1, 2023 when the filer has or reasonably expects to have a CBMA tax benefit assignment from the foreign producer and expects to file a refund claim with TTB based on the assigned lower Internal Revenue Tax (IRT) rate or credit.

Avoiding ACE Data Errors that may Delay Payment of CBMA Importer Refund Claims

See Avoiding ACE Data Errors

myTTB System User Guides

Foreign producer registration and assignment system.

See the Foreign Producer Registration and Assignment System User Guide

Before you register as a Foreign Producer or if you receive an error message when you attempt to register, read this new guidance on common errors.

See the Foreign Producer Registration Common Errors

Importer Claims System

Importer Claims User Guide

Alternate Claims User Guide

General CBMA Import Program FAQs

Gi-1: when do the new cbma procedures take effect.

The new TTB procedures for obtaining CBMA tax benefits apply to merchandise entered for consumption with an Entry Date of January 1, 2023, and after.

GI-2: What can an authorized agent for a foreign producer do?

In TTB’s foreign producer registration and assignment system, an authorized agent for the foreign producer is able to submit and/or edit the foreign producer’s registration information; assign CBMA tax benefits that the foreign producer is eligible to make under law; view all information submitted on behalf of the foreign producer in the system, including information submitted by other authorized persons; receive and respond to communications from TTB regarding the foreign producer; and may also be able to designate additional users depending on the scope of the agent’s authorization. When entering registration or assignment information into TTB’s system, an authorized agent is acting solely as the foreign producer’s agent, and is not acting in their own capacity. The foreign producer and their agents (including any agents who are also importers) are responsible for ensuring that information entered in TTB’s system is accurate and consistent with the foreign producer’s intent.

GI-3: Can a customs broker submit the refund claims to TTB on behalf of a U.S. importer?

An importer may authorize an agent, including a customs broker, to act on the importer’s behalf for purposes of submitting the CBMA refund claim. Generally, TTB importers will be able to grant authorization electronically to third parties through the myTTB system. More information is available on the Getting Started in myTTB page.

GI-4: Do the assignment certification, CBMA spreadsheet, and controlled group spreadsheet that were required in past years also need to be submitted with the refund request to TTB?

In prior years, CBP required three documents that it referred to as an assignment certification, a CBMA spreadsheet, and a controlled group spreadsheet. See, for example, CBP’s message CSMS #50484790 . These were supporting documents for CBMA claims processed under CBP procedures. In general, those requirements applied to goods imported and entered, or withdrawn from a warehouse, for consumption on or before December 31, 2022.

TTB’s procedures for submitting refund claims, starting in 2023, generally rely on information submitted directly through the myTTB system, and TTB does not require the three CBP documents to be created. However, an importer, or its agent, may still be required to submit to TTB the assignment certification, CBMA spreadsheet, and controlled group spreadsheet that were required and created under the CBP procedures in prior years in certain circumstances. For example, TTB may request these documents for claims submitted to TTB with an entry date of January 1, 2023, or later, but an import date prior to January 1, 2023. Additional information on the requirements for claims that fall into this category is available in TTB Industry Circular 2023-1 .

GI-5: If I plan to claim tax benefits, do I have to wait to import products until the foreign producer has registered and made an assignment?

An importer can import the products that will be subject to a refund claim before the foreign producer registers with TTB, obtains a TTB Foreign Producer ID, and assigns tax benefits. However, because the Foreign Producer ID and assignment information will not be available to the importer at the time of entry, the importer will need to update that information in ACE through a post-summary correction prior to filing a refund claim with TTB.

Importer Claims FAQs

Cb-c1: when can i file my claim.

An importer can file a refund claim after the imported products have been entered for consumption in the United States, and after the importer has paid to CBP the tax due on those products.

Additionally, CBMA importer refund claims have a quarterly period. That is, the calendar quarter must end before CBMA refund claims may be filed for any consumption entries made during that quarter. For example, the first day that an importer can file a refund claim for products entered on May 20 is July 1 of that year, because July 1 is the first day after the end of the quarter in which the products were entered for consumption.

Where the first day following the close of a calendar quarter falls on a weekend or holiday, claims for products entered during that calendar quarter may be filed beginning the next business day.

Revised 7/5/23 to add information regarding filing on weekends or holidays.

CB-C2: How do I file a claim?

Importers are required to file CBMA refund claims online through myTTB’s CBMA Importer Claims system. See TTB’s Importer Claims User Guide for step-by-step instructions on filing claims.

CB-C3: I need to provide an importer basic permit number to my foreign producer so they can assign tax benefits to me. However, I am not required to have an importer basic permit. What should I do?

An importer who does not have, and is not required to obtain, an FAA Act basic permit (for example, importers who import only industrial alcohol) must request and receive a reference number from TTB. Contact TTB’s National Resource Center here .

Foreign producers use the reference number to assign tax benefits to the importer. Importers should enter the reference number in place of a TTB permit number when entering import data as part of the importer’s customs entry filing in CBP’s Automated Commercial Environment (ACE).

CB-C4: How long will it take me to get my refund?

TTB envisions that complete and valid claims will be paid shortly after they are filed. However, the myTTB CBMA Importer Claims system relies not only on accurate and complete information being submitted through that system but also on accurate and complete information being submitted electronically as part of the importer’s customs entry filing(s) in CBP’s Automated Commercial Environment (ACE). Inaccurate or incomplete data will significantly delay TTB’s processing of the claim.

CB-C5: Will importers receive a notification when a foreign producer makes an assignment to them?

Currently, the myTTB systems are not designed to send a notification to an importer when a foreign producer makes an assignment of tax benefits to them. However, importers can view all assignments made to them in the myTTB CBMA Importer Claims system.

CB-C6: My CBMA tax benefit assignments from foreign producers are in proof gallons (distilled spirits), wine gallons (wine), and barrels (beer), but I enter my imported quantities in ACE in proof liters or liters. How can I convert my imported quantities to track them against my assignments?

Importers can use the following conversion factors:

Distilled spirits conversion factor: 1 proof liter = 0.264172 proof gallon

Wine conversion factor: 1 liter = 0.26417 wine gallon

Beer conversion factor: 1 liter = 0.008522 beer barrel

CB-C7: I would like to receive my CBMA refund as a check, but I need to update my mailing address. How do I do that?

Users that have an account in Permits Online (PONL) should update the mailing address information in PONL. Users that do not have a PONL account (those with a TTB reference number) will need to contact TTB to correct the mailing address.

Foreign Producer Registration FAQs

Fp-1: what information must a foreign producer provide to register and obtain a foreign producer id from ttb.

Foreign producers seeking to assign CBMA tax benefits must register online through myTTB in order to receive a TTB Foreign Producer ID and assign tax benefits to a U.S. importer. In order to complete the registration process, the foreign producer (or their agent, see FAQ FP-4 ) will need to enter the following information, in the English language, through myTTB .

- Name, country of residence, and principal business address of the foreign producer;

- Name, title, country of residence, phone number, and email address of an employee or individual owner of the business who has authority to act for the business;

- If the person registering the foreign producer is different from the employee or individual owner, the name, address, phone number, and email address of the person who is completing the registration on behalf of the foreign producer; and

- U.S. Food and Drug Administration (FDA) Food Facility Registration Number(s).

Foreign producers who are under common ownership with other foreign or U.S. distilled spirits operations, wineries, or breweries also assigning CBMA tax benefits or taking advantage of CBMA tax benefits (in the case of U.S. alcohol producers) must also provide the following information for any individual or entity that owns 10 percent or more of the registering foreign producer:

- The name, address, and phone number of the individual or entity owner; and

- For entity owners, the Employer Identification Number if the entity is a U.S. entity and has an EIN or the Dun & Bradstreet Data Universal Numbering System (DUNS) number if the entity is a foreign entity and has a DUNS number.

FP-2: What is the FDA Food Facility Registration Number and when is it required as part of a foreign producer’s TTB registration?

The U.S. Food and Drug Administration (FDA) requires foreign beverage alcohol producers to obtain an FDA Food Facility Registration number for their production facilities before their products are imported into the United States. As part of the TTB registration process, foreign producers who seek to assign reduced rates will be required to submit to TTB each FDA Food Facility Registration number that they have already obtained for FDA purposes prior to the importation of their distilled spirits, wine, or beer, into the United States.

In cases where a foreign producer does not have a Food Facility Registration number because all of their products are further manufactured, processed, or bottled by another foreign facility prior to shipment to the United States, the foreign producer must obtain and submit the Food Facility Registration number of the other facility. Alternatively, a foreign producer of industrial alcohol may confirm that it does not have an FDA Food Facility Registration because FDA does not require one for its operations.

FP-3: Who should the foreign producer identify as the “Foreign producer contact” when registering in myTTB?

The foreign producer contact should be an employee or owner of the foreign producer. This individual will serve as the foreign producer point of contact for TTB and should not be the foreign producer’s agent or any other individual or entity acting on behalf of the foreign producer.

Note that this individual will be the recipient of any notices from TTB regarding the foreign producer’s registration or CBMA tax benefit assignments.

FP-4: May a foreign producer use a third party agent to submit its TTB foreign producer registration and CBMA tax benefit assignment information on its behalf?

A foreign producer may have a third party agent register the foreign producer with TTB and make assignments of CBMA tax benefits to importers on its behalf. Once a registration has been created for a foreign producer, no additional registration can be completed for that foreign producer because each foreign producer may only have one registration.

When initially registering the foreign producer, a third party agent must provide basic identifying information about themselves, including their name, address, phone number, and email address. TTB may also request additional information, if necessary, to verify this individual’s identity. Note that, as part of the registration, the agent must still provide a foreign producer contact that is an employee or owner of the foreign producer. See FAQ FP-3 .

A third party agent registering a foreign producer must have authorization from the foreign producer to provide the required registration information, and perform other actions in the myTTB online system, including editing the foreign producer’s registration information, designating additional persons who are also authorized by the foreign producer to act on the foreign producer’s behalf or canceling the designations of authorized persons, and making assignments of CBMA tax benefits. The agent must maintain proof of their authority to act on behalf of the foreign producer, and be able to provide TTB a copy of the documentation authorizing them to make binding commitments on the foreign producer’s behalf. See FAQ FP-6 for additional information on acceptable proof of authority.

FP-5: How and when is a foreign producer required to update their registration information?

Foreign producers who register with TTB are required to update their registration within 60 days of any change to the information that was required as part of the original registration. In addition, every year, the myTTB system will prompt the foreign producer to either confirm or update the ownership information on file with their registration. If the foreign producer fails to confirm or update its registration information, the foreign producer will not be able to assign CBMA tax benefits until the required action is completed.

FP-6: What does a person acting on behalf of a foreign producer need to have as proof of their authorization?

A person acting on behalf of a foreign producer in TTB’s online foreign producer registration and assignment system must maintain written proof of authorization from that foreign producer to act on that foreign producer’s behalf, and must provide that proof to TTB upon request. Proof of authorization from the foreign producer must include the following:

(1) Name and mailing address of the foreign producer, which must be consistent with the name and mailing address for the foreign producer in TTB’s online foreign producer registration;

(2) Name and mailing address of the person whom the foreign producer is authorizing to act on its behalf;

(3) A clear statement by the foreign producer of the scope of authority granted to the authorized person. The foreign producer can either authorize the person to act on its behalf without limitation, or can limit the authorization to perform only the actions listed below. If the latter, the foreign producer must state that the person is authorized to perform each of the following on the foreign producer’s behalf:

(i) Submit and/or edit the foreign producer’s registration information;

(ii) Assign the foreign producer’s CBMA tax benefits to U.S. importers;

(iii) View all information submitted on behalf of the foreign producer in TTB’s online foreign producer registration and assignment system, including information submitted by other authorized persons;

(iv) Receive and respond to communications from TTB regarding the foreign producer; and

(v) (optional) Designate and/or cancel designations of additional persons to act on the foreign producer’s behalf in TTB’s online registration and assignment system.

The proof of authorization must be signed by an individual with authority to legally bind the foreign producer under the laws of the country where the foreign producer is located. This signing individual must attest that they have authority to grant the authorization and must include their printed name, title, and date of signature on the document.

The proof of authorization must also be signed and dated by the individual receiving the authorization to act on behalf of the foreign producer.

FP-7: Does a foreign producer have to designate an agent?

No. Foreign producers can register themselves and make assignments without an authorized agent. If a foreign producer wants to authorize someone else to act on their behalf, the foreign producer can authorize one or more agents. See FAQ GI-2 for what an authorized agent can do on behalf of a foreign producer and FAQ FP-6 for information on proof of authorization.

FP-8: How many registrations can a foreign producer have?

One. A foreign producer can have only one registration, but can authorize multiple agents to access their registration. ( See the Foreign Producer Registration and Assignment System User Guide for a description of user types and their roles and instructions on designating additional persons to act on a foreign producer’s behalf.) If a foreign producer authorizes multiple agents to act on their behalf, each agent must act under the same registration. See FAQ GI-2 for what an authorized agent can do on behalf of a foreign producer.

FP-9: Can a foreign producer who uses several different importers to import their products authorize each of the importers to act as an agent? If so, can each of the importers/agents register through the foreign producer registration system?

A foreign producer can authorize multiple importers to act as agents on their behalf. However, each foreign producer can have only one registration and all of the agents authorized to act on behalf of the foreign producer must use the same registration. See FAQ GI-2 regarding what an authorized agent can do.

FP-10: When I try to register as a foreign producer, I get an error message that says “Registration Error: Registration Incomplete. Due to a potential error, your registration is not yet complete and you have not been assigned a TTB foreign producer ID. After TTB reviews your submission, TTB will either activate your registration in myTTB or contact you by email with additional guidance.” What does it mean?

This error message indicates that your registration information has been received by TTB but your registration is not successful and needs TTB review. This could be due to a number of reasons, including errors with the FDA ID provided in the registration or when there are potential duplicate registrations. TTB will review your submission and will activate it or contact you by email for additional information. If you receive this error message, you will receive a Submission ID, which cannot be used to assign tax benefits. Your Submission ID may also be found next to the foreign producer’s name when you access the registration submission in TTB’s system. You will receive a TTB Foreign Producer ID only when your registration is successful and active in myTTB.

FP-11: Is there a deadline for getting a TTB Foreign Producer ID?

No, there is no TTB deadline for completing foreign producer registration and getting a TTB Foreign Producer ID. However, a foreign producer must complete its registration and obtain a Foreign Producer ID before it can assign tax benefits to U.S. importers, and – starting in 2023 – there are deadlines for making tax benefit assignments. Foreign producers must make their assignments of tax benefits on or before December 31 of the calendar year for which the benefits apply (see FAQ TB-5 ).

See FAQ TB-3 for information on when a foreign producer may assign tax benefits and FAQ NEW GI-5 for information on imports from foreign producers that have not yet obtained a Foreign Producer ID.

CB-FP12: I work with one or more foreign producers. What happens if I register a foreign producer without their authorization?

Any person who registers a foreign producer must have authorization from that foreign producer and must affirm that they are authorized as part of the registration process. If you cannot provide proof of authorization upon request, TTB will inactivate the registration. Any tax benefit assignments made from a foreign producer account created without authorization are invalid. See FAQ FP-6 for information on proof of authorization.

CB-FP13: What should a foreign producer do if they receive a letter from TTB stating that the foreign producer is a member of a controlled group that has assigned more CBMA tax benefits than is permitted by law?

Foreign producers who receive this type of letter should review the assignments they have made in the Foreign Producer Registration and Assignment System and coordinate with other members of the controlled group to identify the corrections that are needed so that the controlled group as a whole does not exceed the annual CBMA quantity limitations. See FAQ TB-2 for more information about how foreign producers that belong to a controlled group must ensure that their combined CBMA tax benefit assignments do not exceed the quantities allowed by law.

Once the controlled group identifies the assignments that need to be reduced, foreign producers who made those assignments must contact the importers to whom they made the assignments, and instruct those importers to return all or part of the assignment. Importers will return the assigned benefits through myTTB’s CBMA Importer Claims System . For more information on returning assignments, see FAQ TB-4 .

If a foreign producer receives this type of letter but disagrees that they are in a controlled group, or disagrees that their controlled group has assigned more tax benefits than is permitted by law, the foreign producer should submit the Controlled Group Inquiry form and a TTB representative will contact the foreign producer.

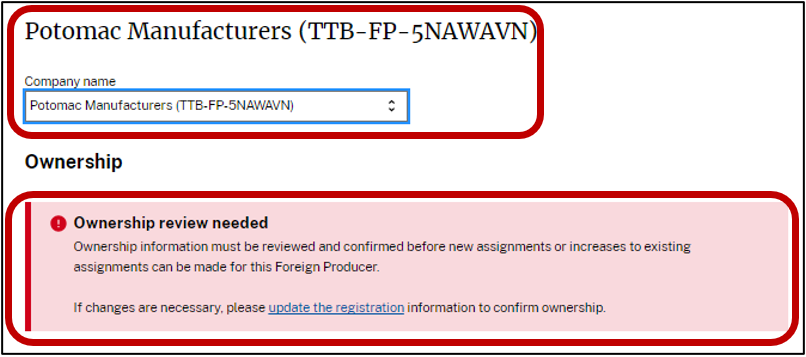

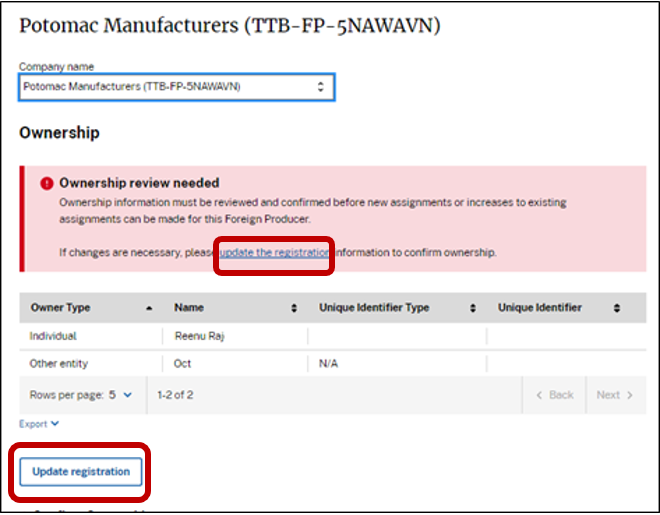

NEW CB-FP14: What is the annual Foreign Producer ownership review and how do I complete it?

TTB's temporary regulations at 27 CFR 27.258 require foreign producers who register with TTB to update their registration within 60 days of any change to information required as part of their original registration. To ensure that this information is current, the myTTB Foreign Producer Registration and Assignment System will prompt the foreign producer to either confirm or update their ownership information on an annual basis.

To complete your review: 1. Go to your myTTB dashboard and select Foreign Producer .

2. Review entity information to ensure you are in the correct account. If ownership review is needed, you will see the “Ownership review needed” message box.

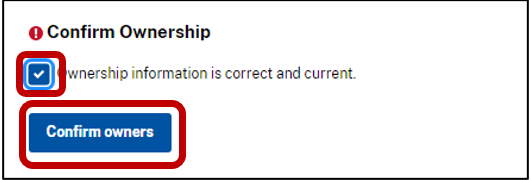

2a. If ownership information is correct and no changes are needed, scroll down to the Confirm Ownership section. Read the statement next to the check box and select the box to agree to the statement. Select Confirm owners .

2b. If you need to make changes to your ownership information, select update the registration or Update registration .

3. Once you select Update registration , update the necessary fields on the Foreign Producer Registration page, including the Foreign Producer Ownership section.

4. Scroll down to the Attestation section. Read the statement next to the check box and select the box to agree to the statement. Select Update registration .

CBMA Tax Benefit Assignment FAQs

Tb-1: what are the quantity limitations on a foreign producer’s assignments of cbma tax benefits.

For distilled spirits, reduced tax rates apply to the first 22,230,000 proof gallons of that foreign producer’s product imported into the United States during a calendar year. These rates are, for each foreign producer, $2.70 per proof gallon on the first 100,000 proof gallons imported, and $13.34 per proof gallon on the next 22.13 million proof gallons imported into the United States.

For beer, a reduced tax rate of $16 per barrel applies to the first 6,000,000 barrels produced by that foreign producer and imported into the United States during a calendar year.

For wine, tax credits apply to the first 750,000 wine gallons of that producer’s product imported into the United States during a calendar year. The credits are, for each foreign producer, $1 per wine gallon on the first 30,000 wine gallons of wine imported, 90 cents on the next 100,000 wine gallons imported, and 53.5 cents on the next 620,000 wine gallons imported. The tax credits are available for all wine, except that CBMA provides for adjusted credits for imported wine eligible for the hard cider tax rate (6.2 cents, 5.6 cents, and 3.3 cents, respectively).

A detailed overview of the tax rates and CBMA tax benefits applicable to imported distilled spirits, beer, and wine is available on TTB's ACE CBMA Tax Rates Table .

TB-2: How does common ownership among producers of distilled spirits, wine, or beer affect CBMA tax benefits for imported products?

A foreign producer that is under common ownership with other foreign and/or domestic producers of beer, wine, or distilled spirits are subject to “controlled group” limitations on the quantities of tax benefits that may be assigned when the common ownership creates a “controlled group” under U.S. law. The Internal Revenue Code provides that the quantity limitations for the CBMA tax benefits are applied to the entire controlled group and shall be apportioned among the members of the controlled group. (See 26 U.S.C. 5051(a)(5)(B), 5001(c)(3)(C), and 5041(c)(3).)

For example, if two foreign wineries whose wine is imported into the United States are in a controlled group with each other (e.g., each is wholly owned by the same corporation), the two wineries are treated as if they are one foreign producer for purposes of applying the quantity limitations on the CBMA tax benefits. In other words, their combined CBMA tax benefit assignments to U.S. importers cannot exceed the quantities allowed by law. See FAQ FP-1 .

The principle applies equally to two or more foreign beer producers in a controlled group and to two or more foreign distilled spirits operations that are in a controlled group.

Similarly, if a foreign beer producer whose beer is imported into the United States is in a controlled group with a U.S. beer producer, the beer produced by the foreign members of the controlled group and imported into the United States and the beer produced and removed by all domestic members of the controlled group are treated as if it were the production and removal of one producer for the purpose of applying the quantity limitations on CBMA tax benefits. In other words, if a foreign producer and a domestic producer are part of a controlled group, the combined removals of their beer into U.S. commerce would be subject to one quantitative limit.

The principle applies equally to a foreign producer of wine that is in a controlled group with a domestic producer of wine as well as to a foreign distilled spirits operation that is in a controlled group with a domestic distiller or domestic distilled spirits processor.

TB-3: When may a foreign producer assign CBMA tax benefits?

A foreign producer will be able to electronically assign CBMA tax benefits through myTTB after they have completed their online registration and received a TTB Foreign Producer ID. In most cases, a Foreign Producer ID will be issued within five business days of completing the online registration. However, inaccurate or incomplete registration information may delay issuance of the Foreign Producer ID.

Under the regulations, foreign producers may assign tax benefits for a calendar year starting no earlier than October 1 of the year prior, and all assignments must be made on or before December 31 of the calendar year for which the benefits will apply. Assignments do not all need to be entered at one time. Foreign producers may assign additional CBMA tax benefits as needed until quantity limitations are reached. To illustrate, a foreign producer could assign a portion of the CBMA tax benefits for its products to be imported in calendar year 2024 on October 1, 2023. The foreign producer could continue to assign CBMA tax benefits for 2024, up to the maximum quantity allowed by law, through December 31, 2024.

TB-4: May a foreign producer reduce the quantity of CBMA tax benefits assigned to an importer or reassign CBMA tax benefits to a different importer?

Once the foreign producer has assigned CBMA tax benefits to an importer, the foreign producer cannot reduce the quantity of the assigned tax benefits or reassign the tax benefits unless the importer to whom the tax benefits were assigned first declines the assigned benefits through myTTB’s Importer Claims system. See the Importer Claims User Guide (page 28) for instructions on how to return an assignment.

The importer can decline the quantities assigned in full or in part. Once the importer has declined the assignment, the foreign producer may reassign the declined benefits through myTTB’s Foreign Producer system. All rules that apply to the timing of assignments apply to reassignments. See FAQ TB-3 .

TB-5: When is the deadline for making assignments?

All assignments for a calendar year must be made by the end of that calendar year. For example, all assignments for 2023 must be made on or before December 31, 2023.

TB-6: Why doesn’t the foreign producer system allow me to assign the maximum quantity of CBMA tax benefits to each of the U.S. importers that import my products?

Each foreign producer has a limited quantity of CBMA tax benefits that they may assign to one or more importers. See FAQ TB-1 for the quantity limitations. The quantity limitation applies to the foreign producer, and it is the maximum quantity that the foreign producer can assign in total. The foreign producer can assign their total quantity of tax benefits to one importer or divide it among multiple importers. All of the foreign producer’s assignments cannot exceed the total quantity of benefits the foreign producer is allowed. The system does not allow a foreign producer to assign, in total, more than the maximum tax benefit the law allows for a foreign producer.

The quantities that a foreign producer can assign may be further limited by common ownership among producers of distilled spirits, wine, or beer. See FAQ TB-2 for an explanation of how common ownership among producers affects CBMA tax benefits. It is the foreign producer’s responsibility to determine their eligibility for CBMA tax benefits in situations where they share ownership with other producers.

TB-7: I am trying to assign tax benefits for wine or beer, but I only see the option for the distilled spirits category. Why is this happening and how do I fix it?

During foreign producer registration, foreign producers must provide an FDA ID or certify, by checking the box shown in the image below, that they do not have an FDA ID because they only produce industrial alcohol. When a foreign producer checks this box, it indicates that they only produce industrial alcohol and the system will only allow them to make assignments for distilled spirits.

If a foreign producer has checked this box in error and limited their account to only distilled spirits assignments, the foreign producer will need to update their registration by unchecking the box shown above, and by providing the appropriate FDA ID(s) as required by TTB’s regulations. See FAQ FP-2 .

TB-8: I pay another company to produce and bottle all of my distilled spirits, wine, or beer for me at their facility. May I assign tax benefits for those products?

No, in this situation the other company is the foreign producer, even if your brand name appears on the labels of the finished products. The other company can register with TTB and make assignments for the distilled spirits, wine, or beer that it produced, including quantities produced under contract with you.

TB-9: May a foreign producer increase the quantity of a CBMA tax benefit assignment made to an importer or importers?

Yes, a foreign producer may increase the quantity of an assignment, up to the limits set by law (see FAQ TB-1 for information on those limits). For step-by-step instructions on increasing an assignment quantity, see Step 4 in the Foreign Producer Registration and Assignment System User Guide .

Note: Foreign producers cannot have more than one assignment with the same importer permit number, calendar year, product category, and tax benefit tier. Instead, the foreign producer will be required to increase the existing assignment to the importer for that calendar year, product category, and tax benefit tier.

For information on how tax benefits can be reassigned after an assignment is returned in whole or in part by an importer, see FAQ TB-4 .

CB-TB10: What happens if a foreign producer does not assign all of their benefits by the end of the calendar year?

If a foreign producer does not assign all of their calendar year tax benefits by the end of that calendar year, they will not have an opportunity in future years to assign those unused tax benefits. By law, each foreign producer may assign a limited quantity of tax benefits for each category of their products imported into the United States (beer, wine, or distilled spirits) during a calendar year. These benefits do not carry over from one calendar year to the next. TTB regulations require that assignments be submitted on or before December 31 of the calendar year for which the CBMA tax benefits are assigned.

NEW CB-TB11: What businesses can register with TTB as foreign producers and assign tax benefits?

TTB regulations define the “foreign producer” who can make CBMA tax benefit assignments as the “foreign distilled spirits operation, wine producer, or brewer.” For CBMA purposes, these terms have the following meanings:

- Foreign wine producer: A foreign entity that produces wine through fermentation or through sweetening, amelioration, the addition of wine spirits, flavoring, or carbonation. A foreign entity that purchases wine in bulk for blending and/or bottling but does not perform any of the production activities listed in the previous sentence may not assign CBMA tax benefits for that wine.

- Foreign brewer: A foreign entity that brews beer through fermentation or produces beer by the addition of water or other liquids during the production process. A foreign entity that purchases beer in bulk for blending and/or bottling but does not perform any of the production activities listed in the previous sentence may not assign CBMA tax benefits for that beer.

- Foreign distilled spirits operation: A foreign entity that produces distilled spirits through distillation. A foreign entity that purchases distilled spirits in bulk for blending, flavoring, and/or bottling may not assign CBMA tax benefits for those distilled spirits. See 26 U.S.C. 5001(c)(3)(B)(i)(I) (limiting the assignment of the tax benefits to the number of proof gallons produced by a distilled spirits operation).

See also TB-8 , explaining that an entity’s brand name on distilled spirits, wine, or beer, does not make that entity the foreign producer for CBMA purposes.

Please send your questions about tax benefits for imports under CBMA using the National Revenue Center Contact Form (choose CBMA in the drop down).

To reach us by phone from 8 a.m. to 5 p.m. EST, Monday through Friday, call 1-877-882-3277, option #3.

Last updated: April 10, 2024

IMAGES

VIDEO

COMMENTS

Learn how the Assignment of Claims Act of 1940 allows contractors to assign moneys due or to become due under a contract to a financing institution. Find out the conditions, policies, and procedures for assignments, no-setoff commitments, and assignee protection.

This clause explains the rights and obligations of the contractor and the government under the Assignment of Claims Act, which allows the contractor to assign its payment rights to a financing institution. It also covers the exceptions, conditions, and procedures for such assignments or reassignments.

31 U.S. Code § 3727 - Assignments of claims. a transfer or assignment of any part of a claim against the United States Government or of an interest in the claim; or. the authorization to receive payment for any part of the claim. An assignment may be made only after a claim is allowed, the amount of the claim is decided, and a warrant for ...

Under the Assignment of Claims Act, a contractor may assign moneys due or to become due under a contract if all the following conditions are met: ( a) The contract specifies payments aggregating $1,000 or more. ( b) The assignment is made to a bank, trust company, or other financing institution, including any Federal lending agency.

52.232-23 Assignment of Claims. As prescribed in 32.806 (a) (1), insert the following clause: (a) The Contractor, under the Assignment of Claims Act, as amended, 31 U.S.C. 3727, 41 U.S.C. 6305 (hereafter referred to as the Act ), may assign its rights to be paid amounts due or to become due as a result of the performance of this contract to a ...

This web page provides the text of a clause that applies the Assignment of Claims Act to federal contracts. The clause explains the rights and obligations of the contractor, the assignee, and the government under the Act.

Subpart 32.8—Assignment of Claims 32.800 Scope of subpart. This subpart prescribes policies and procedures for the assignment of claims under the Assignment of Claims Act of 1940, as amended, 31 U.S.C. 3727 (hereafter referred to as the Act). [48 FR 42328, Sept. 19, 1983, as amended at 51 FR 2665, Jan. 17, 1986] 32.801 Definitions.

232.806 Contract clauses. (a) (1) Use the clause at 252.232-7008, Assignment of Claims (Overseas), instead of the clause at FAR 52.232-23, Assignment of Claims, in solicitations and contracts when contract performance will be in a foreign country. (2) Use Alternate I with the clause at FAR 52.232-23, Assignment of Claims, unless otherwise ...

232.806 Contract clauses. (a) (1) Use the clause at 252.232-7008, Assignment of Claims (Overseas), instead of the clause at FAR 52.232-23, Assignment of Claims, in solicitations and contracts when contract performance will be in a foreign country. (2) Use Alternate I with the clause at FAR 52.232-23, Assignment of Claims, unless otherwise ...

Formerly, assignment of claims against the government had been barred.2 The Act of 1940 enabled lenders to accept as se-curity assignments by contractors of payments due and to become due under such contracts. Banking interests attribute the success of the World. War II V-loan program to the liberalizing effect of the 1940 Act.3.

52.232-23 Assignment of Claims. (a) The Contractor, under the Assignment of Claims Act, as amended, 31 U.S.C.3727, 41 U.S.C.6305 (hereafter referred to as "the Act"), may assign its rights to be paid amounts due or to become due as a result of the performance of this contract to a bank, trust company, or other financing institution, including ...

The Federal Assignment of Claims Act is a crucial piece of legislation that governs the assignment of claims in the federal contracting sphere. With its historical background, purpose and scope, key provisions, and impact on various aspects of business practices, it is essential for all stakeholders to have a comprehensive understanding of this ...

A smart, efficient practice. A relentless focus on problem solving. And an underlying compassion—for our clients and our community. It all adds up to resolutionary thinking. The kind of thinking you can count on from the people of Shulman Rogers. Matthew S. Bergman. (301) 255-0529. Steven W. Walter. (301) 945-9243.

1951-Act May 15, 1951, made it clear that a bank or other financing institution taking an assignment of claims pursuant to this section would not be subject to later recovery by the Government of amounts previously paid to the bank by the assignee except in cases of fraud. 1940-Act Oct. 9, 1940, inserted second and third pars.

Subject to the requirements of the Assignment of Claims Act ( 31 U.S.C. 3727 ), Medicare may pay a government agency or entity under an assignment by the provider. ( 2) Payment under assignment established by court order. Medicare may pay under an assignment established by, or in accordance with, the order of a court of competent jurisdiction ...

1802. (a) In any general assignment for the benefit of creditors, as defined in Section 493.010, the assignee shall, within 30 days after the assignment has been accepted in writing, give written notice of the assignment to the assignor's creditors, equityholders, and other parties in interest as set forth on the list provided by the assignor ...

Under the Government Claims Act, the general rule is that any party with a claim for money or damages against a public entity must first file claim directly with that entity; only if that claim is denied or rejected may the claimant file a lawsuit. (City of Ontario v. Superior Court (1993) 12 Cal.App.4th 894 citing Gov. Code Secs. 905, 945.4 ...

All clauses regarding Assignment are subject to FAR Clause 52.232-23, Assignment of Claims (JAN 1986) and FAR 42.12 Novation and Change-of-Name Agreements, and all clauses governing Assignment ... Contract under any federal fraud statute, including the False Claims Act, 31 U.S.C. §§ 3729-3733. (s) Advertisements and Endorsements.

An assignment or reassignment established by or in accordance with a court order is effective for Medicare payments only if—. ( 1) Someone files a certified copy of the court order and of the executed assignment or reassignment (if it was necessary to execute one) with the intermediary or carrier responsible for processing the claim; and.

Samantha Lewis, Notice and the Claim Presentation Requirements Under the California Government Claims Act: Recalibrating the Scales of Justice , 53 S an D iego L. R ev. 701 (2016). To recalibrate the scales of justice, this Comment advocates for a statutory amendment that encompasses two changes. First, the amendment would require plaintiffs to ...

Moneys due or to become due under the contract described above have been assigned to the undersigned under the provisions of the Assignment of Claims Act of1940, as amended, ( 31 U.S.C.3727, 41 U.S.C.6305). A true copy of the instrument of assignment executed by the Contractor on _____ [Date], is attached to the original notice.

General: For beer, wine, and distilled spirits entered for consumption in the United States on or after January 1, 2023, an importer must pay the full rate of tax to CBP. To take advantage of the CBMA reduced tax rates or tax credits, the importer must electronically file a refund claim with TTB. Importers may file refund claims after the close of each calendar quarter covering their entries ...